From DeFi to NeoFi

The Next Chapter

DeFi

NeoFi

19.2.26

DeFi

NeoFi

19.2.26

Ever since DeFi clicked for me in 2018 while reading Ric Burton's Open Source Banking and Cyrus Younessi's Uniswap — A Unique Exchange, I have been obsessed with the idea that every person on the planet should be able to permissionlessly access or create any imaginable financial product or service. It seemed obvious that the rails to control one's own financial life should be open and accessible to anyone with an internet connection.

But it is now clear that the next phase of the open financial system we've been building for the past decade is not just about helping people bring assets onchain and use them there. The idea that a significant portion of the global population will ever primarily complete the earn, save, and spend loop fully onchain for the majority of their activity is–and perhaps always was–a pipedream.

It's not because we won't get the majority of people using onchain financial products. We will.

It's because due to deeply engrained social, psychological, and commercial inertia, the right solution at the individual level has never been for most people to bring their financial lives fully onchain and forevermore avoid the closed, permissioned, gatekept legacy financial rails.

It's because the future doesn't look like "DeFi replaces TradFi." It looks like DeFi eats TradFi from the inside out… and TradFi, for its part, reaches into DeFi to grab what it needs. The boundary between the two is dissolving, and the most important products of the next decade will be built squarely on the seam.

The Seam Is the Product

I'm a strong proponent of minimizing dependencies. In an ideal world, every DeFi protocol is a self-contained primitive: no oracles, no governance, no external points of failure. The base layer of open finance should be as robust and dependency-free as we can make it.

But here's what I've come to appreciate more deeply: for the vast majority of users, the friction isn't within onchain systems. Uniswap works. Morpho works. Aave works. The hard part, the part where value leaks, UX breaks, and people give up, is the seam between onchain and offchain. The onramp. The offramp. The moment you need to pay rent with yield you earned in a vault, or deposit your paycheck into a position that earns more than the measly 0.01% your bank offers.

This is what Neo Finance is about: the integration layer between onchain financial systems and legacy financial systems. Not DeFi alone. Not TradFi alone. The connective tissue that makes them work as one.

What Neo Finance Is (and Isn't)

Shout out to The Rollup for pushing the term "Neo Finance" and publishing a comprehensive market map that lays out the landscape across nine verticals, covering over 100 projects. As Andy put it: "Neo finance relies on exogenous yield sources typically offchain from sustainable, Lindy businesses which generate consistent revenue at scale. This is going to be a defining new chapter for DeFi." He's right. It's the right framing at the right time.

But let me sharpen it a bit, because I think the boundaries matter.

Neo Finance is not a pure DeFi protocol that lives entirely onchain. Uniswap is DeFi. Morpho is DeFi. These are extraordinary achievements, and they'll continue to be the engine room of the open financial system. But they're not Neo Finance.

Neo Finance is not a CeFi exchange or traditional fintech that gives customers the ability to buy and sell crypto assets held in omnibus accounts. That's just a legacy exchange with new assets.

Neo Finance is the category of products and services that intentionally bridge onchain and offchain financial systems, giving users the benefits of both: the permissionlessness, composability, and transparency of DeFi combined with the familiarity, regulatory clarity, and real-world connectivity of traditional finance.

The key characteristics:

- Core financial use cases: savings, spending, lending, investing, not just trading and speculation

- Onchain self-custody or self-custodial elements: users maintain verifiability of and meaningful control over their assets

- Seamless, low-cost links to traditional rails: debit cards, ACH, SEPA, wire transfers, bank accounts

- Hybrid by design: not apologetically straddling two worlds, but intentionally building for both

The biggest opportunities in crypto's next chapter are not in making purely onchain systems marginally better. They're in the hybrid space, where the open financial system meets the closed one, and where the friction of moving between them is finally eliminated.

The Integration Is Already Happening

If you're paying attention, Neo Finance isn't a prediction. It's already here, accelerating faster than most people realize.

Coinbase × Morpho is the canonical example. In January 2025, Coinbase launched crypto-backed loans powered by Morpho. Millions of Coinbase users can now borrow USDC against their BTC at ~6% interest rates, with the lending happening onchain through Morpho's protocol, while the user experience is pure Coinbase: familiar, regulated, and accessible.

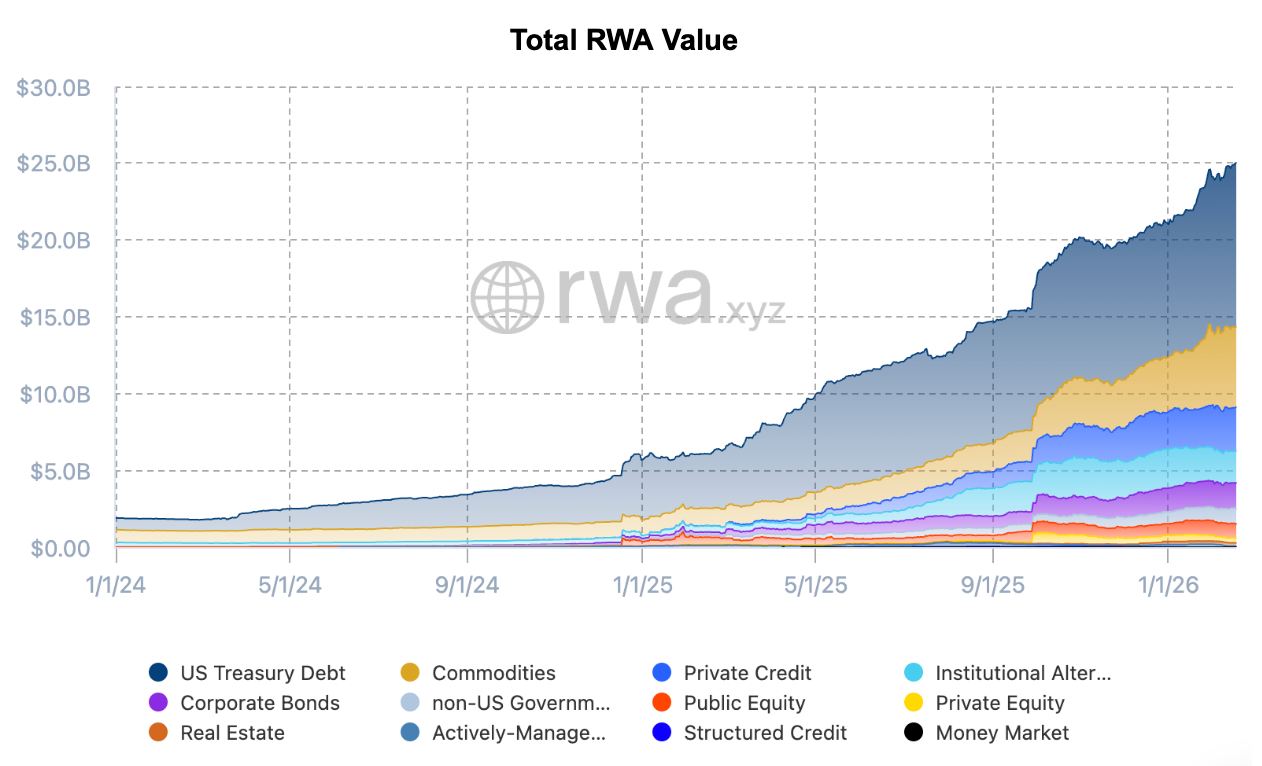

The numbers tell the story. Coinbase has originated over $1.2 billion in USDC loans through this integration, with $800M+ currently active and over $1.4 billion in cbBTC collateralized on Morpho. Morpho itself now holds $5.8B+ in TVL across Ethereum, Base, and Arbitrum, with over $3.3B in active loans. And Coinbase isn't the only one: Bitget, SafePal, and Crypto.com have all integrated Morpho as their onchain lending backend. And let’s not forget a certain $900B asset manager who just quietly announced a massive collaboration and strategic investment.

This is what it looks like when the seam dissolves. The user doesn't need to know what Morpho is. They don't need to bridge assets, manage gas, or interact with a smart contract. They just get a better financial product than their bank could ever offer, powered by open, permissionless infrastructure under the hood.

Tapping into offchain liquidity is another major theme. The deepest liquidity pools in the world are offchain, and the smartest Neo Finance products are building bridges to them rather than pretending they don't exist.

Ethena is the biggest proven example. The idea of a basis-trade-backed synthetic dollar wasn't new; others had tried it purely onchain and couldn't achieve the depth, safety, or scalability needed. Ethena's breakthrough was its willingness to use CeFi exchange liquidity as core infrastructure rather than treating it as the enemy. Equally important was the team's obsessive investment in the operational infrastructure to make it work at scale: a reserve fund, real-time attestations, custodian diversification, and deeply liquid mint/redeem mechanics. The result is $7B+ in TVL, and USDe became the fastest digital dollar asset to reach $10B in circulation.

USD.ai takes a different approach to the same principle. Rather than tapping crypto exchange liquidity, USD.ai brings real-world financing yields onchain. The protocol makes GPU-backed loans to AI infrastructure companies at 15-25% target rates, then wraps that offchain revenue stream into a tokenized product accessible to anyone onchain. It's now at $660M+ in TVL and growing fast.

Tenbin applies the same logic to commodities and currencies, using CME futures markets for minting and liquidation rather than trying to bootstrap onchain liquidity from scratch. OpenFX does it for FX settlement, hedging through futures markets 100x more liquid than spot, enabling real-time settlement with $20B+ in annualized payment volume. And stablecoin neobanks like ether.fi Cash and KAST are closing the loop on the other end, giving users a "checking account" experience with 5%+ yields powered by DeFi on the backend, connected to debit cards and ACH on the frontend.

Why Now?

Stablecoins have achieved escape velocity. The total market cap exceeds $300 billion. Stablecoins processed an estimated $35 trillion in transaction volume in 2025. B2B stablecoin payments grew 733% year-over-year. Interactive Brokers, Stripe, Fidelity, and PayPal are all building stablecoin infrastructure. For years, people asked "what's the killer app?" It was always right in front of us: digital dollars that anyone can hold, send, and earn on, without asking permission.

Regulatory clarity is emerging. Stablecoin legislation has passed. Banks and institutions now have clearer pathways for digital asset interactions, as regulators like the OCC, FDIC, and Federal Reserve retract restrictive guidance and approve custody, settlement, staking, and stablecoin issuance. Globally, frameworks like the EU’s MiCA and those in Japan, Hong Kong, and the UK prioritize reserves, transparency, and risk management. The ambiguity that paralyzed builders is giving way to workable frameworks. This matters enormously for Neo Finance, because these products inherently touch both regulated and unregulated systems.

The infrastructure is ready. Modern L1s and L2s are cheap. Account abstraction is real. You can build a product today that onboards a user with an email, gives them a smart wallet, connects to their bank account, deploys their savings into a Morpho vault, and lets them spend the yield with a debit card. Two years ago, that was science fiction. Today, it’s impossible to keep track of all the teams that are shipping it.

What This Means for Builders

Stop pretending offchain doesn't exist. The purist vision of a fully onchain world is beautiful and worth pursuing at the protocol layer. But at the product layer, your users live in the offchain world. They have bank accounts, pay taxes, receive paychecks, and buy groceries. The products that win will be the ones that meet users where they are and make the onchain/offchain boundary seamless, if not fully invisible.

Tap into offchain liquidity and demand. Tenbin using CME futures for tokenized assets. Ethena using CeFi exchange liquidity for its synthetic dollar. USD.ai channeling AI infrastructure financing yields onchain. The deepest liquidity and most durable yield sources in the world are offchain. Building onchain products that can access them is a superpower, enabling greater reach and more robust markets.

Think about the full customer lifecycle. It's not enough to assume your user already has crypto assets onchain. How are they acquiring or minting assets onchain in the first place? What are they doing with them once they're there? When and why do they need to move back offchain? How do you make every transition seamless? The Neo Finance winners will think holistically about the entire journey, not just one leg of it.

Security remains existential. I've written extensively about this. As Neo Finance expands the attack surface by bridging onchain and offchain systems, every integration point is a potential vulnerability. The products that earn institutional trust and mainstream adoption will be the ones that take security as seriously as they take growth.

The Opportunity

Nascent has been investing in and around this thesis for years. Our portfolio is full of companies building the Neo Finance stack:

- Morpho — $5.8B+ TVL, powering Coinbase's crypto-backed loans and a growing roster of institutional integrations

- Ethena — $7B+ TVL, synthetic dollar protocol bridging CeFi and DeFi yield

- USD.ai — $660M+ TVL, bringing real-world AI infrastructure financing yields onchain

- Tenbin — tokenizing commodities and currencies using existing futures markets for real liquidity

- OpenFX — onchain FX settlement with $20B+ annualized payment volume

- Superstate — $1.4B in tokenized treasury and investment products for institutional adoption

- Birch Hill — institutional onchain credit infrastructure, curating risk-rated lending vaults on Morpho to give fiduciaries compliant access to DeFi yield

The common thread isn't that they're "DeFi" or "TradFi" companies. It's that they're building at the seam, creating products and infrastructure that make the two systems work together better than either could alone.

The Bigger Picture

Here's what I keep coming back to: crypto was never supposed to be a parallel universe. The original promise wasn't to build a financial system that only works for people willing to abandon the existing one entirely. It was to build tools that give everyone more control, more access, and more freedom in their financial lives.

For a while, we got lost in the purity of it. We told ourselves that everything had to be onchain, trustless, and fully decentralized or it didn't count. And at the protocol layer, I still believe that. Primitives should be as robust and dependency-free as possible.

But at the product layer? The layer where real humans interact with real money to solve real problems? The right answer has always been hybrid. Meet people where they are and give them something meaningfully better than what they had before, even if the underlying architecture doesn't satisfy every cypherpunk's ideological purity test.

Neo Finance is the recognition that the most impactful thing we can do is not to replace the legacy financial system overnight, but to make it porous. To create so many integration points between onchain and offchain that the distinction eventually stops mattering. To build products so good that people use them without knowing or caring that there's a blockchain involved, and yet benefit from the permissionlessness, transparency, and composability that only open systems can provide.

This sector will produce more genuine billion-dollar companies than any previous crypto cycle, not because of speculation, but because of utility. Real products, solving real problems, for real people.

The tech is here. The regulatory window is open. The infrastructure is ready. The partners are willing. The only thing missing is more builders who see the opportunity and are prepared to relentlessly execute.

If you're building at the seam between onchain and legacy finance, reach out. We want to back you. And we want to build this future together.

The pie is about to get a lot bigger. Let's grow it.

.jpg)